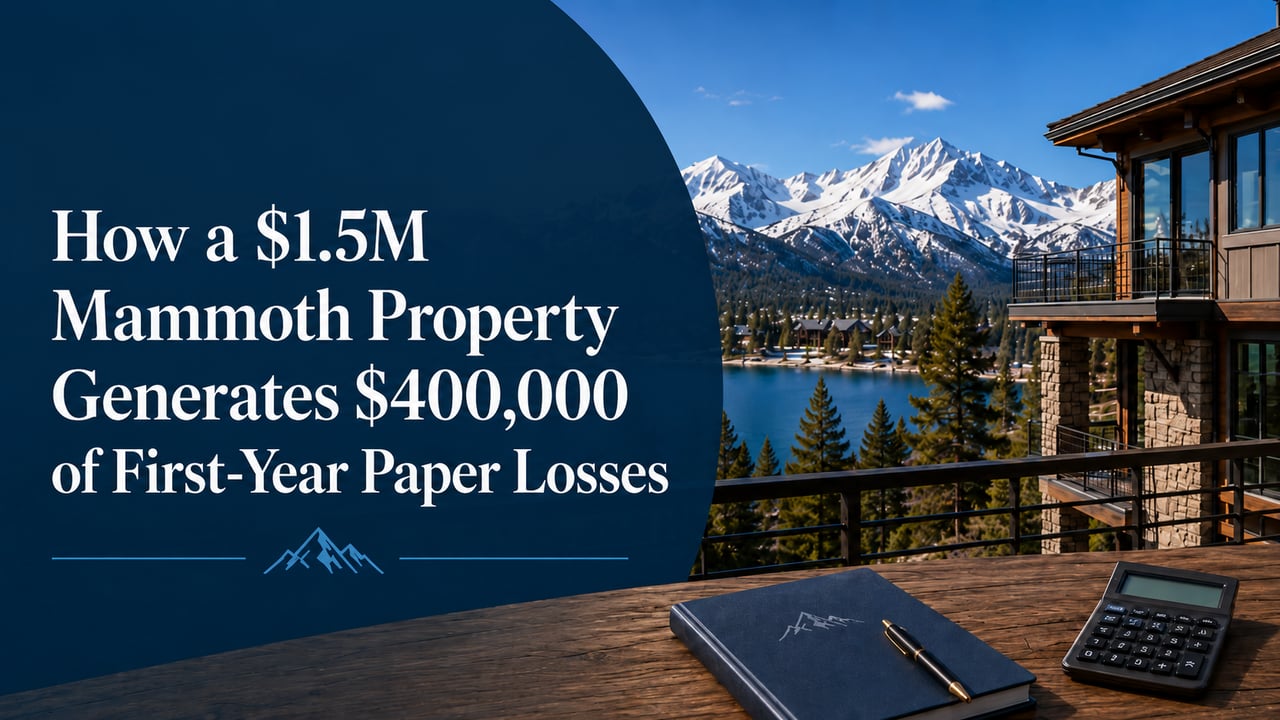

The STR Tax Loophole, Explained: A Buyer's Guide for Mammoth Lakes

May 20, 2026

investing

May 20, 2026

investing

Guest post by Brian Flint, Founder of Highline Hosting — Part 2 of 3

In Part 1 of this series, we walked through what the STR tax loophole actually is, the material participation rules that make it work, and the kind of buyer it fits. That piece was the concept.

This one is the math.

If you are a Destination Real Estate client considering a Mammoth purchase with the STR strategy in mind — or if you are simply trying to figure out whether the numbers you have heard tossed around at dinner are real — this is the post to read carefully. It is also the one I would forward to your CPA before your first conversation with them.

We will walk through a worked example on a $1.5M Mammoth property: how a cost segregation study identifies hundreds of thousands of dollars of short-life basis, how 100% bonus depreciation converts that basis into a Year-1 deduction, how the deduction lands at different income levels, and the half-dozen things that can quietly break the math if no one is watching.

A friendly heads-up before we dive in — I am not a CPA, an attorney, or a tax advisor, and nothing in this post is tax, legal, or financial advice. Everything below is education from the property-management side of the house, written to help you walk into your CPA conversation with sharper questions and a clearer picture of the math. Please give the full disclaimer at the bottom of this post a read before acting on anything here. And if you would like introductions to STR-experienced CPAs and cost segregation specialists we trust and work with regularly, just ask — happy to make the connection.

When you buy a property, the IRS lets you deduct its cost over time through depreciation. Residential rental real estate is depreciated over 27.5 years. That means on a $1.5M Mammoth condo, a standard depreciation schedule gives you roughly $33,000 to $40,000 of deduction per year for 27.5 years.

That is the default. It is also leaving an enormous amount of deduction on the table.

A cost segregation study is an engineering-based analysis that opens up the building and identifies which components of the property are not actually 27.5-year property. The IRS allows certain components to be depreciated over much shorter useful lives — 5 years, 7 years, or 15 years — when they are properly classified.

The components that get reclassified include things like:

5-year property: appliances, carpeting, window treatments, certain cabinetry, decorative lighting, specialty millwork.

7-year property: furniture, fixtures, certain equipment (relevant for a furnished STR rental).

15-year property: site improvements — driveways, decks, landscaping, fencing, exterior lighting, snowmelt systems, hot tub pads.

A qualified cost segregation specialist — typically an engineering firm or a CPA practice with an in-house engineer — visits the property (or works from drawings and site documentation), measures and inventories the qualifying components, and produces a report that allocates your basis across the asset classes.

For a typical Mammoth condo or single-family STR in the $1M–$2M range, that report commonly reclassifies 20% to 30% of the building's depreciable basis into 5-, 7-, and 15-year buckets.

That is where the math starts to move.

Before we get to the numbers, it is worth being precise about what a cost seg study is actually doing — because the most common confusion when a buyer reads the math is mistaking the 27.5-year line item for "what you get if you skip the bonus depreciation." That is not what it is.

The IRS divides the building basis of a residential rental property into two categories, by statute:

Structural components. The building shell — foundation, framing, roof, exterior walls, the HVAC system, the structural plumbing and electrical service. The parts of the building that make it a building. These have to be depreciated over 27.5 years for residential rental property. Always. A cost seg study cannot move them. Bonus depreciation does not apply to them. They are locked in by statute.

Non-structural components. Appliances, cabinetry, flooring, decorative lighting, window treatments, furniture, exterior site improvements (decks, landscaping, snowmelt systems, hot tub pads), specialty millwork. These have shorter useful lives under the IRS asset classification system — 5, 7, or 15 years. These are what a cost segregation engineer goes hunting for.

What the study actually does is carve the non-structural components out of what would otherwise be a single 27.5-year lump and reclassify them into their proper shorter-life buckets. That reclassification is what makes them eligible for bonus depreciation. The structural shell stays on the 27.5-year schedule no matter how aggressive the study is.

Said differently: the cost seg study does not create deduction. It moves deduction from a slow bucket (27.5 years, spread out over decades) into fast buckets (5-, 7-, and 15-year, eligible for Year-1 acceleration). Without the study, the entire building basis sits as 27.5-year property and gives you roughly $40,000 to $44,000 per year of depreciation. With the study, the non-structural buckets get peeled off — and from there, bonus depreciation does the rest of the work.

That mental model is the thing to hold onto as you read the table in the next section. Three rows: two short-life buckets (the carved-out non-structural components, eligible for full Year-1 expensing) and one long-life bucket (the residual structural basis, which keeps depreciating on the standard 27.5-year schedule). All three buckets exist no matter what — the study just changes their proportions, and bonus depreciation determines how fast the short-life buckets land.

The reason a cost seg study matters so much in 2026 — as opposed to a few years ago when bonus depreciation had been phasing down — is that 100% bonus depreciation has been restored for property placed in service after January 19, 2025.

Bonus depreciation lets you deduct the full value of qualifying short-life property in the year it is placed in service, instead of spreading those deductions over the 5-, 7-, or 15-year life.

For a Mammoth STR buyer, this is the engine of the strategy. Without bonus depreciation, the cost seg study would still help — you would just spread the accelerated buckets out over their useful lives, which produces a smoother but smaller Year-1 number. With 100% bonus depreciation back in effect, the entire short-life basis is deductible in Year 1.

That is what produces the headline number buyers hear at cocktail parties. It is also what creates the urgency to actually understand the rules before you close.

Let us put real numbers to this. Assume the following:

Run the numbers:

If the property also includes capitalized improvements you make in your first year — a furniture package, a hot tub, a refreshed bathroom, exterior staining — those are typically eligible for the same bonus depreciation treatment in their own right. A $40,000 furniture and FF&E package alone pushes the Year-1 number past $400,000.

That is the headline figure. Roughly 25% to 30% of the purchase price as a Year-1 deduction is a reasonable rule of thumb for a Mammoth property in this band when the cost seg is done well and the placement-in-service timing is clean.

A $400,000 deduction is not $400,000 in your pocket. It is $400,000 off your taxable income. What that is worth depends on your tax bracket, how much active income you have to offset, and — importantly for Mammoth buyers — how your state handles bonus depreciation.

Two clarifications worth making before the table:

Bonus depreciation is a federal provision, not a state one. The 100% Year-1 acceleration is governed by federal tax law. Most states conform to it automatically, but a handful do not — and California is one of the notable non-conforming states. For a CA-resident Mammoth buyer, the full $400,000 Year-1 deduction lands on your federal return. Your California return follows a slower, traditional schedule.

California still allows cost segregation, just without the Year-1 acceleration. A cost seg study still helps for CA purposes — the 5-, 7-, and 15-year buckets still depreciate faster than the 27.5-year default — but you cannot expense them in a single year on your CA return. The Year-1 CA deduction on the same property typically lands around $65,000–$80,000 rather than $400,000. Over the subsequent years, the additional CA deductions continue to flow as the short-life buckets depreciate down. The total state deduction over the life of the property is roughly the same as federal — just spread out instead of frontloaded.

Here is the same $400,000 federal paper loss translated into cash savings at a few different household income profiles. The "Federal Tax Savings" column is the headline number. The "Approx. CA Year-1 Tax Savings" column reflects the no-bonus reality on a CA return — much smaller in Year 1, with additional state deductions flowing over the following years.

A few things to notice:

The federal deduction is the engine. Even in states that fully conform to bonus depreciation, your state marginal rate is usually a fraction of your federal rate. The headline number is almost always federal.

California non-conformity creates a tracking burden, not a lost deduction. Because federal and CA depreciation diverge starting in Year 1, your CPA will maintain two separate depreciation schedules for the property — one federal, one CA — every year going forward. Modern tax software handles this without drama, but it is worth knowing that "the math" is two sets of books, not one.

Out-of-state Mammoth buyers fare differently. Nevada, Texas, Florida, and Washington have no state income tax, so a buyer resident in one of those states gets no state benefit and no state burden. Most other states conform to federal bonus depreciation in some form. Your CPA can tell you specifically how your home state treats it.

The deduction is most valuable at the top of the federal bracket. That is why this strategy is most often paired with high-W-2 professionals, business owners with strong K-1 income, or dual-earner households with combined income well into six figures.

The deduction has to land in a year where you can use it. If your active income in 2026 is only $150,000, a $400,000 deduction will absorb your active income and leave a roughly $250,000 net operating loss that carries forward. That is not a loss of money — the carry-forward has real value in future years — but it changes the urgency of the Year-1 number.

A good STR-experienced CPA will model exactly this on your specific return before you sign the cost seg engagement.

Three things commonly trip up the math after a buyer is already deep into the transaction.

1. The land allocation. The IRS does not let you depreciate land — only the building and its improvements. If your CPA uses an aggressive 10% land allocation and the IRS later argues it should have been 25%, you have just lost 15% of your depreciable basis. Most cost seg specialists pull a defensible land allocation from county records or from the cost seg engineering analysis itself. Push back on a CPA who is willing to wing it.

2. Placement-in-service timing. The depreciation clock does not start on your closing date. It starts on the date the property is "placed in service" — meaning ready and available for rental use, with the listing live or imminent. A property that closes in May but does not list until October has a placement-in-service date in October, not May. That compresses your Year-1 partial-year convention and shortens the runway for clearing material participation. Sequence the listing and the close together.

3. The interaction with passive loss rules. This is where Part 1 of this series comes back into play. A $400,000 deduction on an STR is only non-passive — only able to offset your W-2 income — if you actually clear material participation in Year 1. If you do not, the deduction still exists, but it lands as a suspended passive loss that cannot offset W-2 income. It sits on your return until you generate other passive income or sell the property. The cost seg report does not care whether you participated. The IRS does.

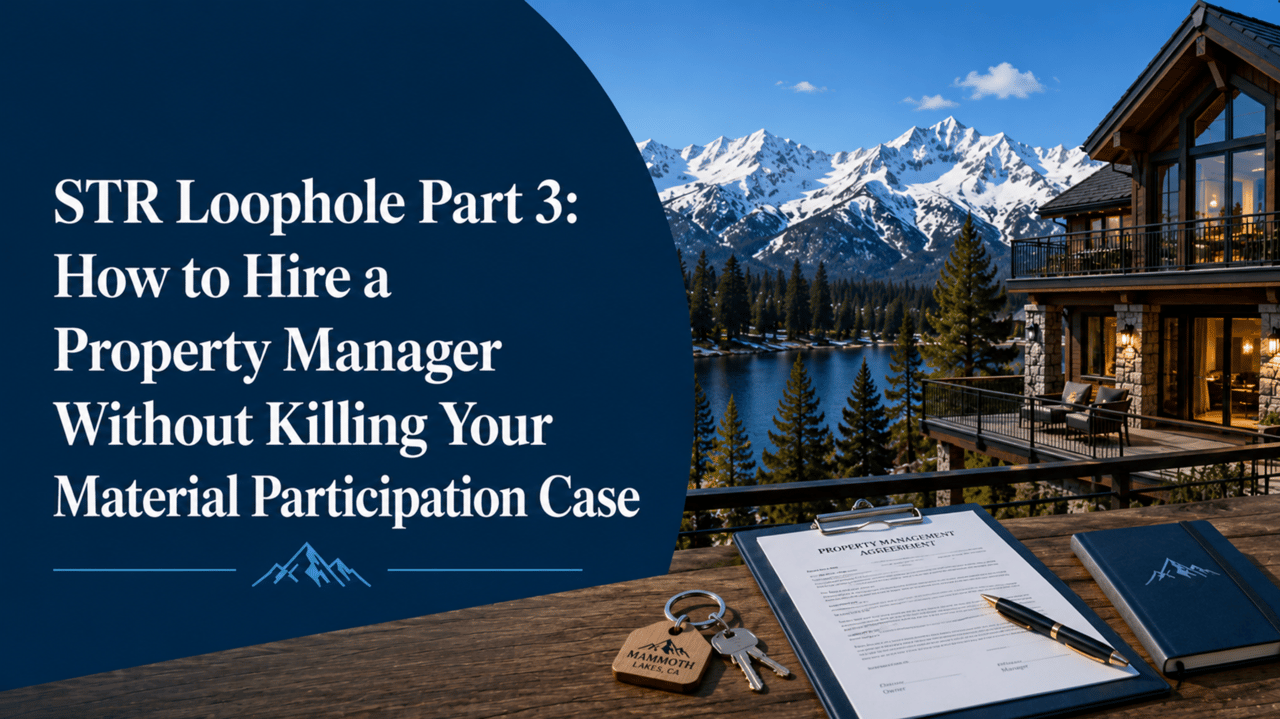

This is why the cost seg conversation and the property management conversation are inseparable. We will cover the operational side of that conversation in Part 3.

If you are working through this with a CPA — and you should be, before you close, not after — here is what they will need to model your situation accurately:

The estimated purchase price and your target close date.

A realistic land allocation for the property (or an instruction to use a defensible engineering allocation from the cost seg).

Your projected active income for the year of close — W-2, K-1, self-employment, business income, and your spouse's income if filing jointly.

Your projected passive income, including any other rental properties or pass-through investments.

Your participation plan — how you intend to clear the 100-hour, more-than-anyone-else material participation test for the property.

The cost seg specialist's preliminary scope — most reputable firms will provide a free benefit estimate before you commit to the full engagement.

If your CPA cannot model this in a spreadsheet in front of you and tell you what the deduction is worth on your specific return, it is worth getting a second opinion from a CPA who has taken multiple clients through this strategy. We are happy to make introductions.

If you are a Destination Real Estate client thinking through any of this — or trying to figure out whether the property you are looking at can realistically support the participation case once it is operational — Highline Hosting is the operational and tax-strategy resource Sonja points clients to on the property-management side.

We have walked through this math with dozens of Mammoth buyers, and we have a short list of STR-experienced CPAs and cost segregation specialists we trust and refer clients to regularly. If you would like an introduction — or a property-specific conversation about whether the numbers work on the specific listing you are considering — Sonja can make the introduction directly, or you can book a call with our team.

For deeper reading on the two strategic paths most Mammoth buyers consider — co-managing from day one or self-managing in Year 1 and transitioning in Year 2 — see our two-part series on the property-management side of the strategy: Part 1: Can You Hire a Property Manager and Still Qualify for the STR Tax Loophole? and Part 2: Self-Manage in Year One, Hand Off in Year Two.

This is Part 2 of a three-part series. Part 3 will cover the operational side of the strategy — specifically, how to choose a property manager whose structure protects the material participation case rather than quietly destroying it.

I am not a CPA, an attorney, or a tax advisor. Nothing in this article is tax, legal, or financial advice — it is education from the property-management side of the house. The §469 material participation rules, what qualifies as participation, and how cost segregation interacts with bonus depreciation are nuanced and fact-specific. Tax laws also change. Always sit down with a qualified CPA or tax attorney before acting on any of the strategies discussed here. If you would like introductions to STR-experienced CPAs and cost segregation specialists we trust, just ask — we work with several and are happy to make the connection.

Brian Flint is the founder of Highline Hosting, a boutique short-term rental management company serving Mammoth Lakes, Park City / Deer Valley, and Blue Ridge GA. Highline works closely with Sonja Bush and Destination Real Estate as the trusted operational and tax-strategy resource for short-term rental buyers across these markets.

Brian Flint — Founder, Highline Hosting highlinehosting.net | [email protected] | (760) 965-3863 Instagram: @flinthighline | Facebook: Highline Hosting

Stay up to date on the latest real estate trends.

Buyer

June 18, 2026

Buyer

June 16, 2026

Market Update

June 9, 2026

Buyer

June 2, 2026

June 1, 2026

Part 3 of 3 Part Series

Real Estate Education

May 28, 2026

Market Update

May 26, 2026

May 21, 2026

investing

May 20, 2026

Part 2 of 3 Part Series

You’ve got questions and we can’t wait to answer them.