Saving Up For a Home Down Payment and Closing Costs

April 2, 2018

Real Estate

April 2, 2018

Real Estate

The next step in preparing for your home purchase is to save up for a down payment and closing costs.

Down Payment

When you purchase a home, you typically pay for a portion of it in cash (down payment) and take out a loan to cover the remaining balance (mortgage).

Many first-time buyers wonder: How much do I need to save for a down payment? The answer is … it depends.

Generally speaking, the higher your down payment, the more money you will save on interest and fees. For example, you will qualify for a lower interest rate and avoid paying for mortgage insurance if your down payment is at least 20 percent of the property’s purchase price. But what if you can’t afford to put down 20 percent?

On a conventional loan, you will be required to purchase private mortgage insurance (PMI) if your down payment is less than 20 percent. PMI is insurance that compensates your lender if you default on your loan.1

PMI will cost you between 0.3 to 1.5 percent of the overall mortgage amount each year. So, on a $100,000 loan, you can expect to pay between $300 and $1500 per year for PMI until your mortgage balance falls below 80 percent of the appraised value. For a conventional mortgage with PMI, most lenders will accept a minimum down payment of five percent of the purchase price.1

If a five-percent down payment is still too high, an FHA-insured loan may be an option for you. Because they are guaranteed by the Federal Housing Administration, FHA loans only require a 3.5 percent down payment if your credit score is 580 or higher.1

The downside of getting an FHA loan? You’ll be required to pay an upfront mortgage insurance premium (MIP) of 1.75 percent of the total loan amount, as well as an annual MIP of between 0.80 and 1.05 percent of your loan balance on a 30-year note. There are also certain limitations on the types of loans and properties that qualify.2

There are a variety of other government-sponsored programs created to assist home buyers, as well. For example, veterans and current members of the Armed Forces may qualify for a VA-backed loan requiring a $0 down payment.1 Consult a mortgage lender about what options are available to you.

| TYPE | MINIMUM DOWN | ADDITIONAL FEES |

| Conventional Loan | 20% | Qualify for the best rates and no mortgage insurance required |

| Conventional Loan | 5% | Must purchase private mortgage insurance costing 0.3 – 1.5% of mortgage annually |

| FHA Loan | 3.5% | Upfront mortgage insurance premium of 1.75% of loan amount and annual fee of 0.8 – 1.05% |

Current Homeowners

If you’re a current homeowner, you may have equity in your home that you can use toward your down payment on a new home. We can help you estimate your expected return after you sell your current home and pay back your existing mortgage. Contact us for a free evaluation!

Closing Costs

Closing costs should also be factored into your savings plan. These may include loan origination fees, discount points, appraisal fees, title searches, title insurance, surveys and other fees associated with the purchase of your home. Closing costs vary but typically range between two to five percent of the purchase price.3

If you don’t have the funds to pay these outright at closing, you can often add them to your mortgage balance and pay them over time. However, this means you’ll have a higher monthly payment and pay more over the long term because you’ll pay interest on the fees.

Sources:

Stay up to date on the latest real estate trends.

Real Estate Education

May 28, 2026

Market Update

May 26, 2026

May 21, 2026

investing

May 20, 2026

Part 2 of 3 Part Series

Investing

May 12, 2026

Part 1 of 3 Part Series

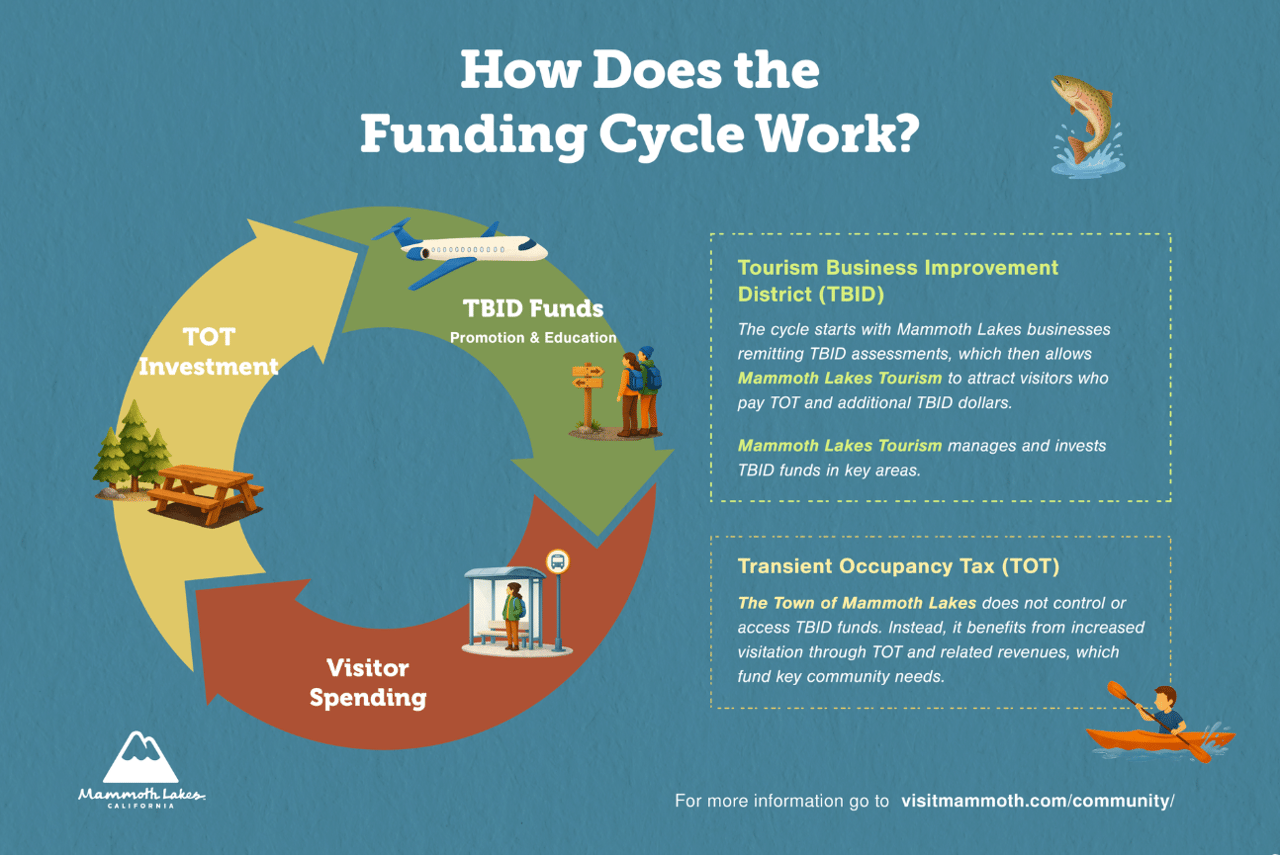

Mammoth Lakes Community

May 11, 2026

Buyer

April 24, 2026

Buyer

April 23, 2026

Market Update

April 6, 2026

You’ve got questions and we can’t wait to answer them.